On March 18, 2022, I had the privilege to attend the General Membership Meeting of the American Chamber of Commerce of the Philippines, entitled “BSP Economic Briefing: The Philippines in 2022”. They have invited no less than the governor of the Bangko Sentral ng Pilipinas (BSP), Gov. Benjamin Diokno.

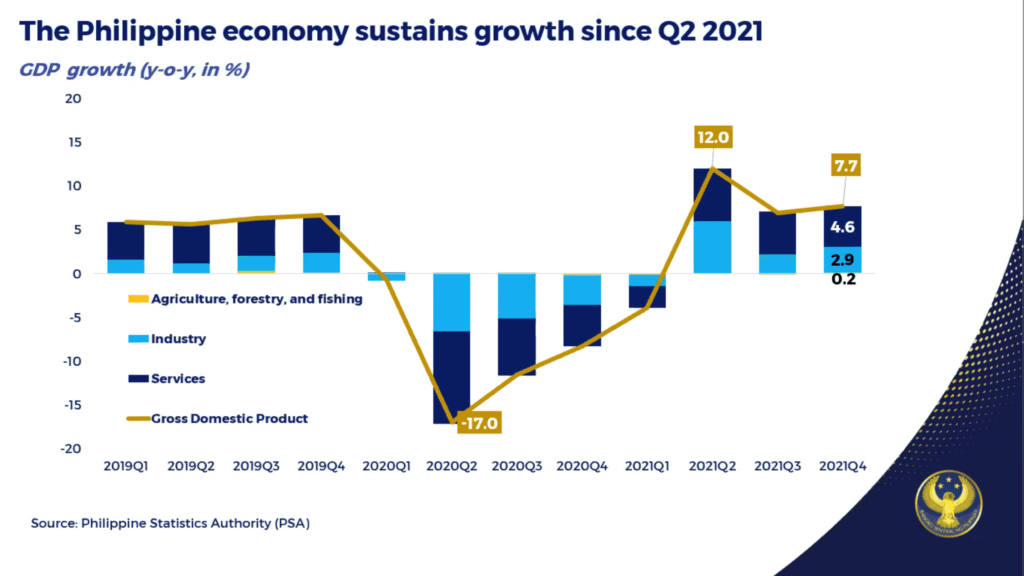

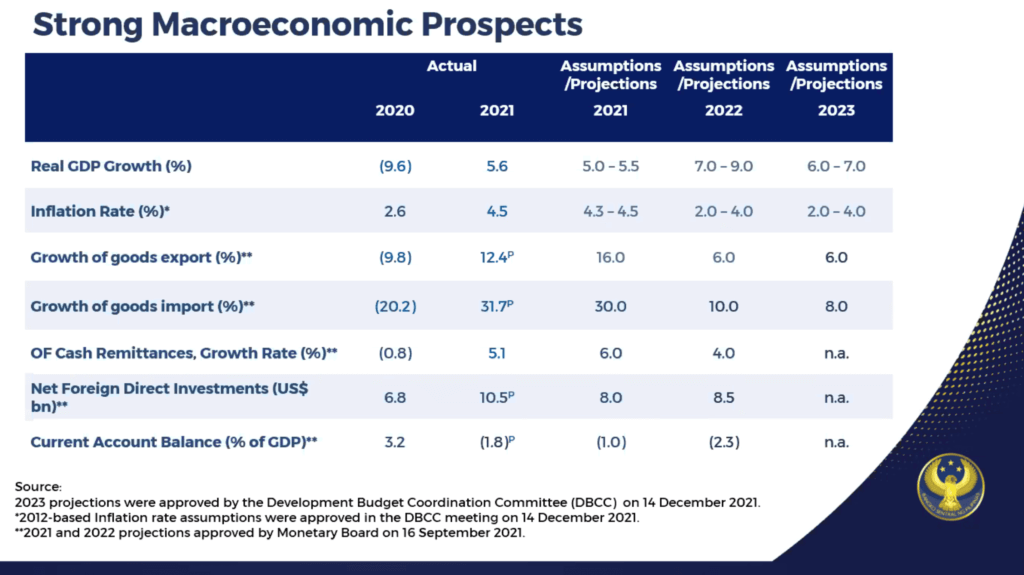

The Philippine economy had only bounced back in the second quarter of 2021, after five succeeding years of decline, sporting a growth rate of 12%, which has been maintained since then. Additionally, the country’s economy saw an upturn of 7.7%, resulting in a 5.6% full-year growth rate, which, according to Gov. Diokno, is above the government’s target of 5%–5.5%

Moreover, Gov. Diokno highlighted that the country has witnessed an improvement in its employment situation over the last few years, citing that the unemployment rate had decreased to 6.4% in the first month of this year, in comparison to April 2020’s peak of 17.6%. Similarly, the 43.02 million employment posted in January 2022 represented a 1.77 million net employment gain from January 2021.

In addition, manufacturing activities were also said to be gaining traction. The purchasing manager’s index increased by 1.3% to a three-year high of 52.8 in February 2022, following the loosening of restrictions and quarantine protocols.

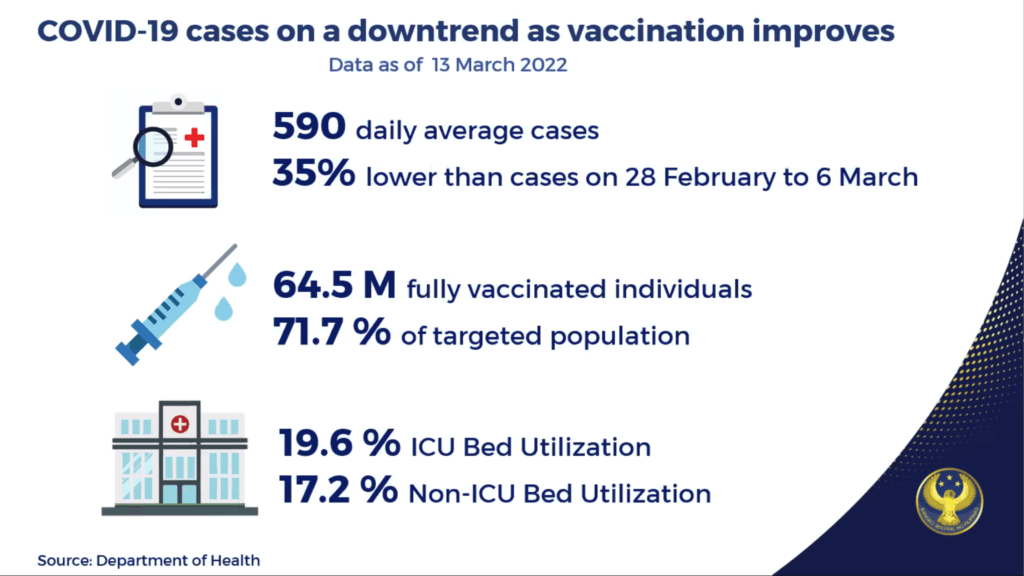

In line with this, it was mentioned that the COVID-19 situation is improving as confirmed cases continue to decrease by the day. The vaccination rate is rising and, in turn, the hospitalization rate is declining.

Headline inflation stood at 3% in January and February 2022, the midpoint of the government’s average inflation target range of 2%–4% for the year. According to Gov. Diokno, inflation expectations remained well-anchored as inflation projections from private-sector economists and multilateral agencies for 2022, 2023, and 2024 are all within the government’s target range of 2%–4%.

Adding on, the country’s external sector remains manageable as the sustained rebound in key economies continues to spur external demand. FDIs rose by 54.2% to USD10.5 billion in 2021, reflecting positive investor sentiment and indicating great opportunities for job creation. OFW cash remittances and BPO revenues grew 15.1% and 9.5% year-on-year, respectively, in 2021.

Backed by strong foreign exchange inflows, gross international reserves stand hefty at USD108 billion as of end-February 2022. This illustrates a more-than-adequate external liquidity buffer tantamount to 10.2 months of imports of goods, payments for services, and primary income. It is also about 8.4 times the country’s short-term external debt based on original maturity and 5.8 times based on residual maturity.

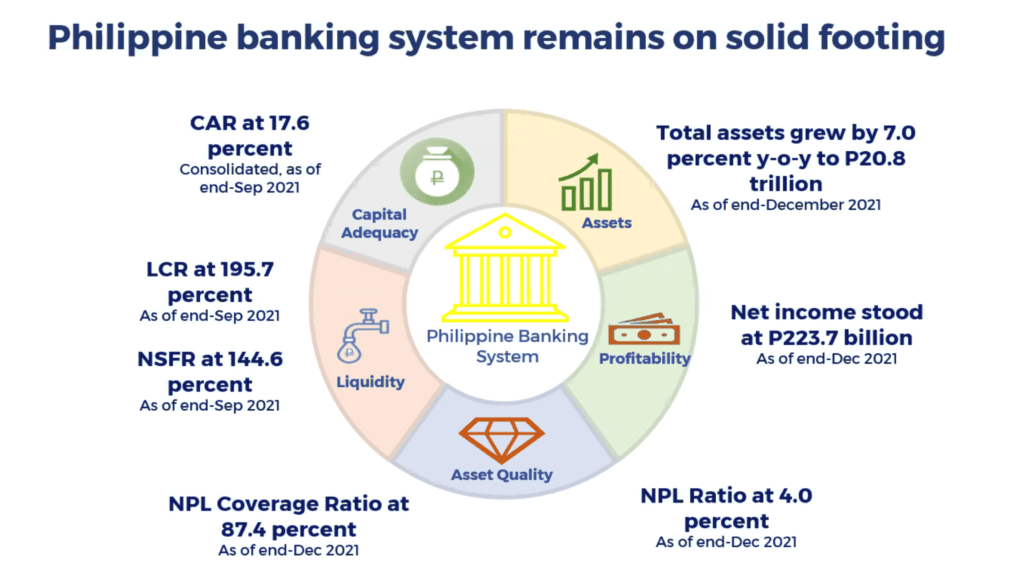

The Philippine banking system has remained sound and stable, as shown by continued growth in assets, deposits, and capital, as well as net profit, stable capital and liquidity buffers, ample loan loss reserves, and manageable loan quality. Overall, the banking system’s financial condition allows it to contribute to and aid in the country’s financing needs.

Likewise, bank lending has posted six consecutive months of year-on-year growth since August 2021, rising to 8.5% in January 2022.

As far as pandemic recovery measures are concerned, the economy is well on its way to recovery as a result of swift and decisive moves. On the part of the national government, it has passed the Bayanihan 1, Fist Act, CREATE, and has allocated an appropriate portion of the 2021 and 2022 national budgets to the vaccination program. On top of that, the 2022 GAA also contains fiscal stimulus. In addition, it was mentioned that the implementation of COVID-19 measures will help the economy bounce back.

On the part of the BSP, they have implemented a long list of crisis responses—from actions intended to boost market confidence to extraordinary liquidity measures. With their liquidity-easing measures, the BSP has allotted about PHP2.2 trillion (approximately USD42.9 billion), equivalent to 11.1% of the country’s GDP, into the financial system. They have also implemented regulatory and operational relief measures to maintain the stability of the said system and in ensuring public access to related services.

Also, amid the consecutive waves of downgrading from developed and emerging countries, credit rating agencies have maintained the Philippines’ investment-grade credit ratings throughout the pandemic, reflecting their confident approach to the Philippine economy’s recovery prospects.

As the recovery further gains traction, BSP has begun considering its exit strategy. This involves recalibrating our monetary operations, unwinding our liquidity provision, reducing monetary accommodation (when prospects for the economy have improved), and building our buffers in preparation for future crisis episodes. Currently, the BSP’s key policy rate remains at a historic low of 2%. The low-interest-rate environment has contributed to the support of credit activities amid the pandemic. However, some groundwork for the BSP’s “exit” had already been initiated with the significant decline in the BSP’s purchases of government securities in the secondary market since the latter part of 2020 and the reduction in the provisional advances to the national government from PHP540 billion to PHP300 billion.

Gov. Diokno also shared the country’s economic outlook, stating that after a higher-than-target growth of 5.6% last year, government projects for the Philippine economy will grow by 7%–9% this year, and by 6%–7% next year. Meanwhile, the latest baseline inflation forecasts are within the target range at 3.7% for this year and 3.3% for next year. In recent weeks, there has been heightened uncertainty caused by the continuous increase in world crude oil prices. Based on the BSP’s oil price simulation, however, inflation could settle above the target range of 2%–4%, only if crude oil prices average higher than USD95 per barrel in 2022 and 2023 on a sustained basis. If prices stand below USD95 per barrel, inflation will settle within the target range. In the case that oil prices reach USD120–USD140 per barrel this year, inflation would be 0.7–1.0 percentage points above baseline in 2022. To summarize, inflation would average between 4.4%–4.7% under the USD120–USD140 per barrel situation.

Meanwhile, the current account is expected to post a deficit equivalent to 2.3% of the GDP in 2022 as it is being pushed by the rising demand for imported capital goods and inputs for production while the economy is on the road to recovery. Overseas Filipino remittances are expected to grow at 4% this year, following a 5.1% growth in 2021—a pattern that suggests resilience. Meanwhile, net foreign direct investments are projected to rise to USD8.5 billion this year, amid improved domestic and global investment climate expectations.

Gov. Diokno highlighted that the BSP has been continuously working for the enactment of structural reforms, which include the following:

- The amended Retail Trade Liberalization Act (signed into law last December 2021) lowers the minimum paid-up capital for foreign retailers

- The amended Foreign Investments Act (signed into law on March 2, 2022) encourages professionals to bring in their practice, know-how, and technical expertise to the Philippines

- The amended Public Service Act (approved by Congress and waiting for signing by the President) will open key economic sectors like telecommunications, airline industries, among others

Gov. Diokno also admitted that there are risks to this outlook. One is the uneven recovery between advanced economies (AEs) and emerging market economies (EMEs), since the pace of mass vaccination and the effectiveness of policy support are contradicting. Another risk is the potential emergence and spread of new COVID-19 variants in other countries. Rising inflation, both in AEs and EMEs, is also a threat owing to growing demand, input shortages caused by supply chain bottlenecks, and rapidly rising commodity prices.

Furthermore, the BSP expects the conflict between Russia and Ukraine to continue exerting pressure on key commodity prices, particularly oil and wheat. According to Gov. Diokno, the conflict may also affect global trade and investment outlook and be the cause of financial market volatility.

I am optimistic that the economic recovery will continue. The BSP is committed to helping the national government achieve full recovery. The gradual reopening of the economy has helped revive household consumption, which has resulted in a rekindling of business sentiment. This is also an election year and election-related spending may indeed support economic activity. I am just hoping that the Filipinos would elect the right leader for the country! It is crucial for us to have a new president with the right vision for the country—someone who would be able to sustain this economic growth.

Please visit and join the John Clements Talent Community.