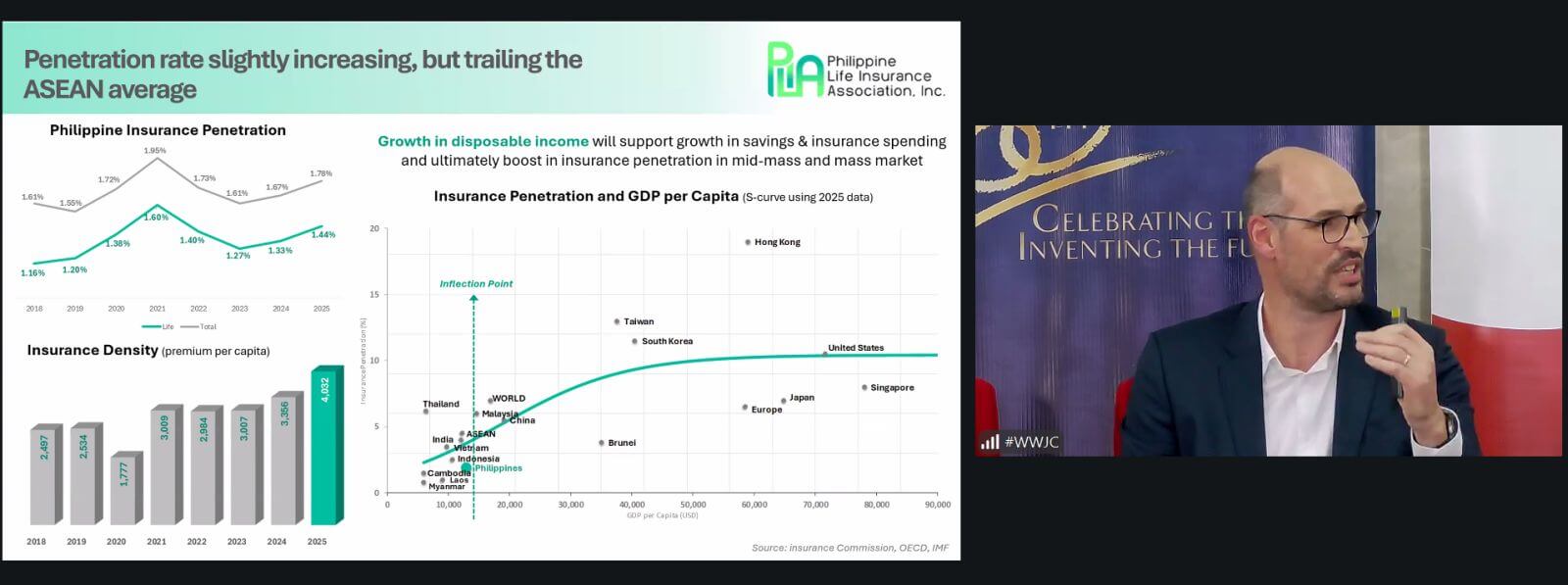

The Philippine life insurance industry is standing at a crossroads. With premiums surging by 14.5% in 2025—far outpacing GDP growth—the sector is showing resilience and momentum. Yet penetration remains at just 1.78% of GDP, trailing ASEAN peers and underscoring the need for deeper financial inclusion, stronger trust, and innovative solutions.

This was the central theme of the Insurance Industry Outlook – Navigating Risk and Change briefing held on March 5, 2026, featuring Sjoerd Smeets, CEO and President of EastWest Ageas Insurance, alongside panelists George Mina of the Philippine Life Insurance Association (PLIA) and Jared Uichico of KRM Reinsurance Brokers Philippines. Their insights painted a vivid picture of both the opportunities and challenges shaping the industry.

Growth Outpacing the Economy

Life insurance remains the backbone of the Philippine insurance sector. In 2025, total premium income reached ₱403 billion, with life insurance accounting for the majority. This growth rate—nearly triple the GDP’s 4.7%—signals strong consumer demand for protection and savings products.

Yet despite this expansion, penetration remains low compared to regional averages. According to the Insurance Commission, only 28% of Filipinos currently hold life insurance policies. This gap highlights the urgency of building awareness and affordability, especially among younger demographics and gig workers who represent emerging segments of the economy.

Shifting Consumer Preferences

The briefing emphasized how consumer behavior is reshaping product demand. Rising healthcare costs—expected to jump 18.3% in 2026—have made health and critical illness coverage top priorities. With 44.4% of medical spending still out-of-pocket, Filipinos increasingly view insurance as a financial safety net.

At the same time, traditional guaranteed products are regaining popularity. In 2025, their share of new business annual premium equivalent (NBAPE) rose from 52% to 55%. High interest rates and weak stock market returns have driven consumers toward products with guaranteed benefits and shorter pay periods, such as 2-pay variants and single-pay products.

Insurers are responding with innovation: flexible variable universal life (VUL) funds, sector-linked investments, and embedded insurance partnerships with fintechs like Singlife x Maya. These offerings aim to meet diverse needs while expanding reach.

Digitalization and Financial Inclusion

Digital transformation is reshaping the industry’s operating model. Between 2020 and 2025, digital payments grew at a 30% compound annual growth rate, reducing friction in premium collection and claims disbursement. Merchant payments now account for nearly 65% of digital transactions, while person-to-person transfers are rising thanks to QR Ph and mobile banking (Bangko Sentral ng Pilipinas).

Insurers are also leveraging artificial intelligence to modernize processes. AI tools now guide agents on product suitability, coach them on customer engagement, and automate underwriting. Companies like SunLife and InLife have adopted ALLFINANZ SPARK, a SaaS solution that streamlines underwriting and improves efficiency.

Financial literacy programs are another pillar of inclusion. Initiatives such as FWD Ignite Financial Dreams and EastWest Ageas PURPLE Solutions aim to equip Filipinos with the knowledge to make informed financial decisions. Meanwhile, the introduction of takaful insurance in 2024 has opened doors for Shariah-compliant products, with the market projected to reach ₱23 billion by 2033.

Regulatory Shifts on the Horizon

The industry is also preparing for the adoption of IFRS 17 by 2027, a new accounting standard that will fundamentally change profit recognition. IFRS 17 requires insurers to measure future cash flows, risk adjustments, and contractual service margins, leading to more volatile profit-and-loss statements.

Only 11 insurers are currently fully ready for this transition, underscoring the scale of the challenge. Dual reporting requirements and potential impacts on shareholder equity will demand significant investment in systems and talent.

Challenges That Demand Action

Despite strong growth, the industry faces persistent challenges:

- Affordability: Most Filipinos have emergency funds capped at ₱100,000, limiting their ability to invest in insurance.

- Trust: Consumers still rely heavily on family and friends for financial advice, highlighting the need for credible advisors and transparent communication.

- Resilience: Geopolitical risks and volatile investment climates require insurers to diversify portfolios and explore alternative assets.

- Penetration Gap: At 1.78%, the Philippines lags behind its ASEAN peers, underscoring the critical importance of inclusion and innovation.

Opportunities for Transformation

The panelists emphasized that the future lies in embedding insurance into everyday life moments. Whether through digital platforms, bank assurance partnerships, or bundled products, insurers must make coverage accessible and relevant.

Generational shifts also present opportunities. Younger, digital-native Filipinos are more open to app-based insurance and financial planning. By tailoring products to their needs—flexible coverage, living benefits, and shorter pay terms—insurers can capture a new wave of customers.

Innovation will be key. Parametric insurance for climate risks, wearable-driven underwriting, and AI-powered personalization can help insurers deliver value while protecting the middle class.

Building Trust, Expanding Reach

The Philippine life insurance industry is at an inflection point. Growth is strong, but penetration remains low. To unlock its full potential, insurers must balance affordability with innovation, strengthen trust through transparency, and leverage digital platforms for inclusion.

As Sjoerd Smeets and the panelists highlighted, the path forward is not just about selling policies—it’s about building confidence, protecting families, and enabling financial resilience. In a country where only 28% of people hold life insurance, the opportunity is vast.

The challenge is to make insurance not just a product, but a trusted partner in every Filipino’s financial journey.

Stay in the know. Follow John Clements Consultants on LinkedIn to keep updated on upcoming industry briefings, insights, and thought leadership pieces that shape the future of insurance and workforce development in the Philippines.